Skilled Nursing Costs Without Medicare Coverage

Compare private pay, LTC insurance, Medicaid, Medicare Advantage, and VA options for nursing home costs when Medicare won't cover.

Skilled nursing care is expensive, and Medicare often doesn’t cover what people expect. By 2026, the average cost of a private room in a nursing home is $135,528 per year, with higher rates in areas like Florida’s South Walton region. Without Medicare footing the bill, families face five main payment options:

- Private Pay: Simplest but most expensive, with costs rising annually.

- Long-Term Care Insurance: Reduces costs but requires early planning and premiums.

- Medicaid: Covers full costs but has strict eligibility rules and limited facility options.

- Medicare Advantage/Supplemental Plans: Helps with short-term costs but has coverage limits and network restrictions.

- VA Benefits: Offers reduced or free care for eligible veterans based on service history and disability ratings.

Each option has trade-offs in terms of cost, eligibility, and facility access. Early financial planning is critical to managing these expenses effectively.

1. Private Pay

Out-of-Pocket Costs

Paying directly from personal savings is straightforward but expensive. By 2026, the national median cost for a private room in a nursing home is projected to be $11,294 per month (or $135,528 per year), while a semi-private room averages $9,842 per month (or $118,104 per year). Costs can vary significantly depending on location. For instance, Alaska has the highest average at $15,600 per month, while Oklahoma offers the lowest at $6,200 per month. To put this into perspective, a $300,000 asset base would cover about 48 months of care in Oklahoma but only 19 months in Alaska. On top of these base rates, additional costs for supplies, therapies, medications, and personal amenities might apply. While the payment process is simple, the financial burden can be steep and unpredictable.

Eligibility Complexity

One of the biggest perks of private pay is its simplicity: there are no eligibility requirements. Unlike Medicare, which necessitates a qualifying three-day hospital stay, or Medicaid, which enforces strict income and asset limits, private pay only requires the ability to cover the costs. There’s no paperwork, waiting periods, or financial scrutiny involved.

Facility Choice

Private pay offers the broadest range of facility options. While not all nursing homes accept Medicaid, nearly all welcome private-pay residents. In some cases, rates are even negotiable, especially when facilities are trying to fill vacancies or when families can make upfront payments. This flexibility is particularly helpful when seeking top-rated facilities or specialized care, such as memory care for Alzheimer’s or dementia, which can add $1,500 to $3,500 per month to the base rate.

"When you're on Medicaid, the state will say, 'We have an available bed in this facility within your region.' You'll go there, and you'll be sharing a room with one or two other people, and that's it." - Chris Orestis, President of Retirement Genius

Predictability of Costs

Although initial rates are clear, they often increase annually. Facilities typically review care needs each year, and costs can rise as health conditions evolve.

"Typically on an annual basis, they'll reevaluate if you need more services or not. Sometimes that happens as we age. Sometimes that happens as maybe somebody has a fall or an illness." - Shanna Reed, Financial Planner

Nursing home costs are climbing at a rate of 3% to 5% per year, outpacing general inflation. Financial planners recommend factoring in a 5% annual increase when estimating how long savings will last, as relying on today’s rates could lead to running out of funds too soon. Additionally, many facilities require a 12- to 24-month private-pay period before allowing residents to transition to Medicaid. To avoid surprises, families should make it a habit to request itemized invoices monthly, as billing errors - like charges for unused supplies - are more common than expected.

Having a clear understanding of these cost factors is crucial when exploring other payment options later in this guide.

Medicare vs Medicaid: Nursing Home Costs Explained #shorts

2. Long-Term Care Insurance

Long-term care insurance (LTCI) is designed to cover the gaps left by Medicare, particularly for extended custodial care that Medicare typically doesn't handle. If you already have a policy or are considering one, here's how it impacts skilled nursing costs.

Out-of-Pocket Costs

LTCI helps reduce, but doesn’t completely eliminate, out-of-pocket expenses. Most policies contribute between $2,000 and $10,000 per month toward care costs. However, with the median cost of a private room sitting at $11,294 per month, there’s often a shortfall you’ll need to cover yourself.

Additionally, most policies include a 90-day elimination period, during which you’re responsible for the costs. At a national median rate of $376 per day, this can add up to approximately $33,840 before your insurance kicks in.

Eligibility Complexity

Before benefits are paid, you must meet specific eligibility criteria. Typically, this involves certification from a licensed professional that you’re unable to perform at least two of the six Activities of Daily Living (ADLs) - eating, bathing, dressing, continence, toileting, and transferring - or that you have a diagnosed cognitive impairment like Alzheimer’s or dementia.

Insurers also apply stringent underwriting standards, often denying applicants with pre-existing conditions such as diabetes with complications, cardiovascular issues, or cognitive decline. The ideal time to apply is between ages 55 and 60, as denial rates rise significantly after age 70. For a $165,000-benefit policy, annual premiums average $950 for a single male and $1,500 for a single female at age 55, increasing to $1,200 and $1,900, respectively, by age 60.

Facility Choice

One of the biggest advantages of LTCI over Medicaid is the freedom to choose your care setting. Policies often cover private nursing homes, assisted living facilities, and even home care, rather than limiting you to state-approved Medicaid facilities. This flexibility is particularly valuable when seeking specialized services, like memory care units or higher-rated facilities.

Predictability of Costs

Hybrid policies - which combine long-term care benefits with life insurance or an annuity - offer guaranteed premiums that remain stable while benefits grow.

In contrast, traditional stand-alone policies are less predictable. Insurers have historically raised rates significantly - sometimes by 100% to 200% - over the life of a policy. Without an inflation protection rider (typically 3% to 5% annual growth), the fixed daily benefit may cover less of your costs as time goes on. The National Council on Aging highlights this key advantage of hybrid policies:

"A hybrid (linked-benefit) policy with inflation protection has a guaranteed premium, meaning your premium will not change - even as your benefit increases."

While LTCI doesn’t entirely remove the financial burden, it can substantially reduce it, especially when paired with inflation protection. Next, we’ll explore Medicaid as an alternative solution.

3. Medicaid

Medicaid serves as the final safety net for those who have exhausted private pay or long-term care insurance options. Unlike Medicare, Medicaid offers coverage for skilled nursing care without a time limit, as long as you meet the necessary medical and income criteria. This makes it a more predictable option for managing long-term care costs compared to the rising fees associated with private pay.

Out-of-Pocket Costs

Medicaid covers 100% of nursing home expenses, including room, board, medications, therapy, and skilled nursing care. However, beneficiaries are required to contribute nearly all their monthly income, keeping only a small personal needs allowance (PNA) of $30–$100. Private rooms are generally not included unless deemed medically necessary, meaning most beneficiaries share accommodations - an important limitation compared to private pay or long-term care insurance.

Once these costs are understood, the next step is navigating Medicaid's strict eligibility requirements.

Eligibility Complexity

To qualify for Medicaid, you must meet both the Nursing Home Level of Care (NHLOC) standard and strict financial criteria. As of 2026, eligibility typically requires having assets under $2,000 and a monthly income below $2,982. Additionally, a five-year look-back period is enforced by most states to prevent improper asset transfers. For those whose income or assets slightly exceed the limits, many states offer a spend-down program. This program allows you to allocate excess resources toward care costs until you meet Medicaid’s thresholds.

Rosalind Newsholme, Program Associate with NCOA's Center for Economic Well-Being, highlights the variability of Medicaid programs:

"While there is some overlap, Medicaid programs tend to be very individual to each state."

Facility Choice

Medicaid only covers care provided by certified Medicaid Nursing Facilities (NFs). Not all nursing homes hold this certification, so if you initially choose a private-pay facility that isn’t certified, you may need to transfer once funds run out. Verifying a facility’s Medicaid certification beforehand is crucial. Tools like Medicare.gov's Care Compare can assist in identifying certified facilities and evaluating their quality ratings.

Predictability of Costs

After meeting eligibility requirements and completing any necessary spend-down process, Medicaid offers a stable cost structure. Beneficiaries are responsible for contributing their income minus the PNA, while Medicaid covers all remaining costs with no time limit. This level of predictability can be a relief compared to the fluctuating costs of private pay options. Understanding how Medicaid operates is essential for planning skilled nursing care without relying on Medicare.

sbb-itb-d06eda6

4. Medicare Advantage and Supplemental Coverage

If you're not eligible for Medicaid but still face high skilled nursing facility (SNF) costs, Medicare Advantage and Medigap supplemental plans can help reduce your out-of-pocket expenses. Here's a closer look at how these plans differ in terms of costs, eligibility, and facility access.

Out-of-Pocket Costs

Under Original Medicare, SNF stays beyond 20 days come with a $217 daily copay, which adds up to about $17,360 for a 100-day stay. A Medigap plan, such as Plan G or Plan N, can cover this entire coinsurance, potentially reducing your SNF costs to $0 during this period - though you'll still need to meet the $1,736 Part A deductible first.

Medicare Advantage plans, on the other hand, set their own cost-sharing rules. While these plans must at least match Original Medicare's coverage, many include an annual out-of-pocket maximum ranging from $5,000 to $10,000 for in-network services.

Eligibility Complexity

Both Medicare Advantage and Medigap are available to those enrolled in Medicare Part A, but they come with different requirements. Medigap plans work alongside Original Medicare and typically require a three-day inpatient hospital stay before SNF coverage begins.

Medicare Advantage plans often waive this three-day rule, allowing you to access SNF care without prior hospitalization - a major benefit if your hospital stay is brief or skipped entirely. However, MA plans frequently require prior authorization, meaning you'll need the plan's approval before starting SNF care. This process can lead to delays or denials. To address these issues, new rules set for 2026 will require Medicare Advantage plans to provide clearer guidelines on these decisions.

"Each MA plan makes its own rules about how much skilled nursing care it will cover, for how long, and under what conditions." - CaringInfo

Facility Choice

Medigap plans offer broad flexibility, allowing you to use any Medicare-certified facility across the country. In contrast, Medicare Advantage plans generally limit you to their in-network providers. If your preferred nursing home isn't in the network, you'll either face higher out-of-network costs or need to switch to a different facility.

"Medicare Advantage plans must offer the same coverage, but some may have specific networks of skilled nursing facilities that you'll need to use to take full advantage of your benefits." - Paul Wynn, Journalist

Predictability of Costs

Medigap plans provide consistent, predictable coverage by filling standardized gaps in Original Medicare year after year. Medicare Advantage plans, however, can change their costs, networks, and prior authorization rules annually. To stay informed, review your plan's Annual Notice of Change (ANOC) by September 30 each year to understand any updates to SNF coverage or cost-sharing rules.

If your Medicare Advantage plan denies SNF coverage that your doctor deems medically necessary, act quickly by filing an expedited appeal. This can help ensure you maintain access to the care you need.

Next, we’ll explore how Veterans Health Administration benefits can offer additional options for managing skilled nursing costs.

5. Veterans Health Administration

For veterans who qualify, VA benefits can significantly reduce or even eliminate skilled nursing costs. Eligibility is primarily based on the veteran's priority group, which is determined by factors like service-connected disability ratings, income, and service history.

Out-of-Pocket Costs

Veterans in Priority Group 1 - those with a service-connected disability rating of 50% or higher - pay $0 in copays for VA care. To put this into perspective, the national median private-pay rate for skilled nursing care ranges from $294 to $330 per day, which adds up to about $120,450 annually. Veterans in lower priority groups may have fixed copays, determined by their income and disability status. Even so, these costs are far below what most private-pay patients face.

"Whether or not you'll need to pay copays - and how much you'll pay - depends on which of our 8 priority groups we assign you to when you enroll in VA health care." - Veterans Affairs

Eligibility Complexity

VA eligibility can be a bit tricky to navigate. The VA is obligated to provide nursing home care to specific groups, including veterans who need it due to a service-connected disability, those with a combined disability rating of 70% or higher, or those with a 60% rating who are considered unemployable. Discharge status also plays a crucial role. Veterans with a dishonorable discharge are disqualified, while those with an "other than honorable" discharge must undergo a Character of Discharge review.

"The VA is required to provide nursing home care to any veteran who needs nursing home care as a result of a service-connected disability [or] has a combined disability rating of 70% or more." - Elyse Futhey, J.D., Nolo

Facility Choice

VA-funded care is available through various facility types, each with its own rules and limitations.

| Facility Type | Managed By | Key Limitation |

|---|---|---|

| Community Living Center (CLC) | Federal (VA) | Admission depends on space and clinical need |

| Community Nursing Home | Private (VA-contracted) | Often limited to 6 months for lower-priority veterans |

| State Veterans Home | State government | VA covers up to 50% of costs; state sets its own rules |

One challenge is geographic availability. If there’s no nearby CLC or VA-contracted facility, veterans may have fewer options.

Predictability of Costs

VA costs are among the most stable compared to other payment methods. Veterans in Priority Group 1 don’t pay copays, while others face fixed rates that don’t fluctuate with market trends. However, factors like bed availability, clinical eligibility reviews, and local service capacity can impact when and where care is provided.

This level of predictability and affordability makes VA care an appealing choice, especially when compared to other options. It’s a strong foundation for evaluating the overall pros and cons of these benefits.

Pros and Cons of Each Payment Option

Skilled Nursing Payment Options: Cost, Eligibility & Coverage Compared

When planning for skilled nursing care without Medicare coverage, it’s important to weigh the pros and cons of available payment methods. Each option comes with its own set of trade-offs, which can significantly impact costs, eligibility, and facility choices. The table below provides a clear breakdown of these factors.

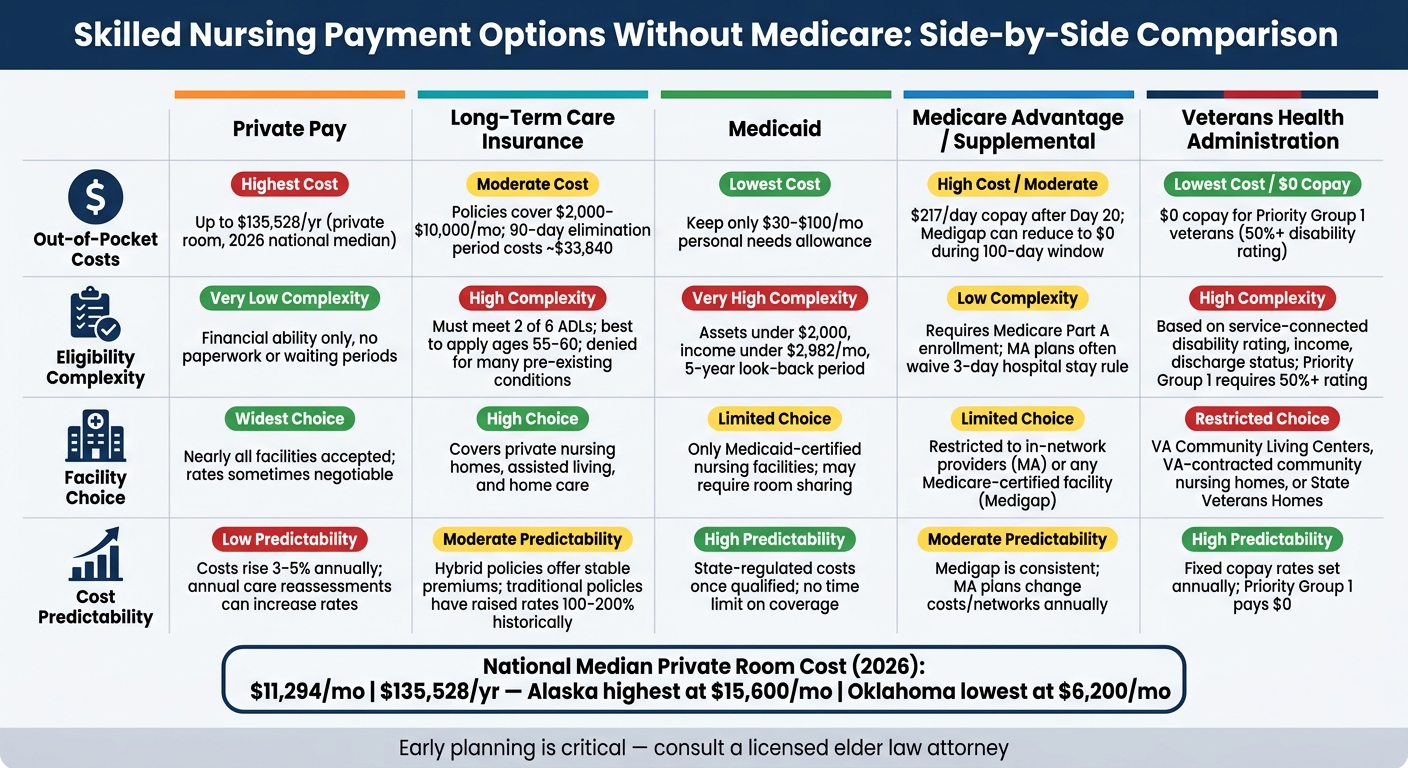

| Payment Option | Out-of-Pocket Costs | Eligibility Complexity | Facility Choice | Predictability of Costs |

|---|---|---|---|---|

| Private Pay | Highest – full market rate | Very low – based solely on financial ability | Widest – nearly all facilities accept this option | Low – subject to annual rate increases |

| Long-Term Care Insurance | Moderate – requires ongoing premiums | High – strict medical underwriting | High – most facilities accept these policies | Moderate – premiums can increase over time |

| Medicaid | Low – mostly limited to a personal needs allowance | Very high – strict asset/income limits and a five-year look-back | Limited – only Medicaid-certified beds available | High – costs are state-regulated once qualified |

| Medicare Advantage / Supplemental | High – $217/day after Day 20 and full cost after Day 100 | Low – requires enrollment in Medicare Parts A & B | Limited – restricted to the plan's provider network | Moderate – fixed copays but with potential coverage denials |

| Veterans Health Administration | Low to none for qualifying veterans | High – based on service record, disability rating, or clinical need | Restricted – limited to VA-operated or VA-contracted facilities | High – pension rates set annually |

Private pay stands out for its flexibility, offering the widest range of facility choices and quicker admission. However, it comes with the steepest costs. Elder law attorney Jason Neufeld highlights this advantage:

"It will generally be easier to enter a nursing home or assisted living facility as a private pay resident first. If you disclose your intent to apply for Medicaid before entry, they may try to discourage admission."

Long-term care insurance provides a middle ground, balancing reduced out-of-pocket costs with broader facility options. However, policies must usually be purchased while still in good health, often in your 50s. Premiums for a $200 daily benefit typically range from $2,000 to $4,000 per year.

Medicaid, on the other hand, is the most affordable option once eligibility is achieved. The process, though, is complex, with strict income and asset limits. In areas like South Walton, Medicaid-certified beds can be scarce, especially in coastal facilities. This limitation can make Medicaid less accessible in high-demand regions.

Geography also plays a significant role in cost variation. Along the Florida Panhandle, daily rates can differ greatly depending on the facility’s location. For residents in areas like South Walton and 30A, this variability makes payment strategies even more important. VA benefits and Medicaid often serve as critical supplements for those unable to afford higher coastal rates.

Each payment method comes with its own set of challenges and advantages, making it essential to carefully evaluate which option aligns best with individual needs and circumstances.

Conclusion

Skilled nursing care comes with a hefty price tag, and Medicare seldom covers long-term needs. For older adults, the financial risk is significant - especially in high-demand areas like South Walton and 30A, where costs are even steeper.

Each payment option has its pros and cons. Private pay gives the most flexibility but can drain savings quickly. Long-term care insurance works best when purchased early, ideally in your 50s, while Medicaid offers strong financial support but requires meeting strict eligibility criteria. VA benefits can bridge some gaps, but early planning is crucial to make the most of these options.

As Florida Medicaid planning attorney Jason Neufeld advises:

"Acting earlier, even a few months before a crisis, dramatically expands the planning options available."

For South Walton and 30A residents, where annual costs range from $105,850 in Panama City to $130,488 in Crestview, high demand not only raises prices but can also lead to long waitlists. Researching facilities that accept Medicaid or participate in the Medicaid Waiver program ahead of time can save a lot of stress later.

To safeguard your assets and secure the care you need, consult with a Florida-licensed elder law attorney. Early planning is essential for residents in this area to navigate the challenges of long-term care effectively.

FAQs

How long will my savings last if nursing home costs increase 5% annually?

If nursing home costs increase by 5% each year, your savings might cover expenses for around 14 to 15 years. This estimate is based on the current median cost of $107,310 annually for a semi-private room. However, this doesn't account for additional factors like personal expenses or potential changes in your income.

What mistakes can delay Medicaid approval or trigger penalties during the 5-year look-back?

When applying for Medicaid, certain financial missteps during the 5-year look-back period can cause significant delays or even penalties. These include:

- Gifting or transferring assets below fair market value: Giving away property or money without receiving full value in return can raise red flags during Medicaid's review.

- Poor documentation of financial transactions: Incomplete or unclear records of financial activities can complicate the approval process.

- Improper use of irrevocable trusts: Mismanaging these trusts or not adhering to Medicaid's guidelines can result in penalties.

To avoid these issues, it's crucial to ensure all financial decisions align with Medicaid's rules and are well-documented.

How do I confirm a skilled nursing facility will accept my coverage before I’m admitted?

To ensure a skilled nursing facility (SNF) accepts your coverage, start by checking if it’s CMS-certified and accepts your insurance, like Medicare or Medicaid. Reach out to the facility directly to confirm they participate in your specific plan. Additionally, verify your eligibility for Medicare-covered services and make sure your medical needs align with the criteria for skilled nursing care before admission.